3 Proven Effective ways to Save Money

Jay and I have always joked about how we don’t really feel inflation that much in the past years because we don’t really have the money for more than the basics, but this time around, we actually experience the consequences of the global economic crisis because even the basics are so expensive.

Our three sons have also grown. I find that it was easier to fix the budget for our expenses when they were younger and smaller, and had simpler joys. Their needs have changed. Nowadays, their expenses are more than just spending for a token or two at the arcade, or a combo meal at their favourite fast food restaurant; now there are bus trips to their trainings to pay for, as well as paying for the training sessions, themselves, not to mention food allowances and clothing expenses. They need expensive computers and programs as part of their education, and don’t get me started on how much they eat!

Think TEENAGE BOYS.

We also found out that because of the pandemic, we now have to occupy two rooms in hotels when we book as a family. Just a couple of months ago, we intended to use a gift certificate at a hotel to celebrate our eldest’s 17th birthday, but we had to pay for another room because COVID protocols are still in place and family rooms for 5 heads have ceased to exist because of it.

A lot of people said that they managed to save some money during the two years of lockdown, but our experience is the total opposite. I found that it was easier for us to splurge more during the lockdown to manage boredom.

We’ve been tiny living for 7 years and while it’s a great lifestyle for people who have access to great places outdoors, it’s not ideal when you cannot go anywhere and your version of tiny living is a 21-square feet, single BR unit on top of a building that sits on a hill and has no yard.

To us, the two lockdown years were chaos! Everyone had to do what they had to do simultaneously in our tiny space. Jay and I were on our laptops, working, the kids were attending their academic classes and would have to reorganise the living room and set it up for their dance classes while me, their dad, and youngest brother would either tuck ourselves away in the tiny bedroom or the narrow balcony for three hours trying to find something to do to bide time. Because they occupied most of the space of our tiny home, often, meals had to be ordered because we can’t cook while they were dancing!

We also bought art materials, books, boardgames, and food (yep, we got fat during the lockdown!) so we had things to do while we sardined in our little abode other than binge on Netflix and YouTube, and Social Media.

Having said all that, I found that there were three very practical, very effective ways to continue saving at any season you’re in, lockdown, inflations or otherwise.

3 Proven Effective ways to save money

1. Set aside money for savings as soon you receive a pay check.

I heard this from many financial gurus, but it’s only been recently that I’ve proven that they were right about this. People tend to save after they’ve paid their bills, but the wise ones say you must set aside money for savings first before you pay your bills. It doesn’t matter how much you’re earning or if you’re a freelancer or an employee who receives your pay fortnightly, decide on an amount and transfer it to your savings account right away!

My husband’s salary has been automated to transfer a small percentage of it to another one of his accounts every month, while I have to manually transfer the same amount to my other bank whenever my employer wires it. And because we’ve made a habit of this, we were able to save despite our increase in expenses and the strong urge to splurge in the last two years.

But did you know that you can actually set goals doing this?

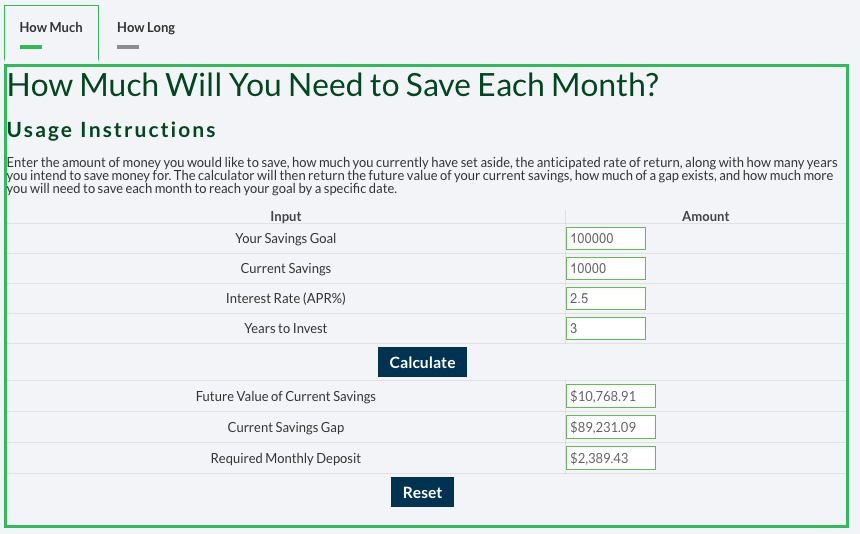

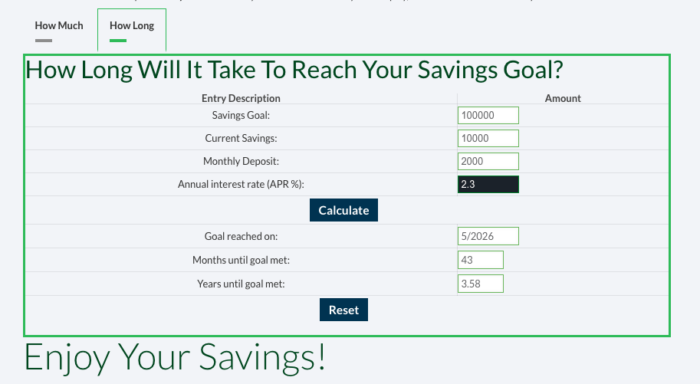

I found this really useful goal calculator that helps me figure out how much I need to set aside each month to reach a financial goal and how long before I achieve it.

Now, take note that the calculator is using USD as the default currency, but as long as you put in the correct figures, like how much you have in your savings now to start, how much your financial goal is, the APR% in your country (you can google this!) and how many years you plan to invest, it will calculate accordingly and show you how much you need to set aside each month and the date when you can finally fulfil this goal.

Check this out:

The first image tells me how much I need to set aside per month to achieve my goal amount in three years; the second image shows me that I will reach my goal by May 2026 if I only plan to deposit that much monthly.

Simple, right? It gives me a clearer picture of how I should plan out and manage my finances.

The goal calculator is only one of the many savings calculator on the site, savingscalculator.org. There is one for education goals and another for retirement goals, and there is the CD investment, all of which are some of the most important financial goals people have.

2. Spend money on good quality products

I used to think that people are just being extravagant when they buy expensive products, but I realise that I can learn something from my more wealthy friends. They don’t buy cheap products, they buy quality ones which usually cost more, but also last longer.

During the lockdown, I started shopping at this popular online store and bought clothing and shoes because they were OH-MY-GOSH-SO-AFFORDABLE! I found out later on that it cost me more because they had to be discarded after a few weeks use, or that they well ill-fitted and uncomfortable. How can a dress fit you perfectly on all parts of your body but your chest??

Now I know to be willing to spend more and buy from trusted online stores instead. One good buy is better than 3 bad purchases.

3. Practice Delayed Gratification

Resist the urge to spend on the spot. What I do is add to my cart first and wait for a week or two, or even a month before deciding to buy it. Sometimes, after delaying a purchase, I find the item less appealing to buy. This gives me the option to set aside and save money for something better.

This goes for anything!

My new bank has an app that gives me the option to set goals such as financial investments, education, real estate, travel, emergency fund and personal goals. Each one has an amount set but that’s more like a guide, you can customise the amount as you please. You won’t be able to touch your money until you’ve reached the goal you’ve set which I think is great because if you apply #1, then, #3 will keep you from withdrawing your money, haha!

I’ve set mine to personal goal for now because I just want a certain amount for savings and I’m still learning how to navigate the app, I’m fairly new to it. But I do plan to set up financial goals to save for emergencies and travel.

The truth of the matter is…!

You don’t really have to start big. You can even start with just $50 as long as you are consistent. Of course, the bigger the money you set aside, the bigger the savings will be, especially if you don’t just keep them in the banks, but to grow them through investments, like in stocks or bonds.

Or you can go for safer investment options like Mutual or Index Funds. The truth of the matter is, if you want to save more, you must aim to earn more. Ideally, earn more with less work. Increasing your income is the best way to save more because how much you save will also depend on how much you’re earning.

What about you, do you have any other ideas on how to save more effectively? Tell me!

20 Comments

Beth

These are excellent tips. Paying yourself first is the best thing you can do for your finances. That’s the only sure way to set money back every month.

Courtney

Great tips! I’ve been trying to save money out of my paychecks!!! Every little bit helps!

knycx journeying

Agree that it’s not about how much you spend but instead, think about it and spend it wisely. It does literally save a lot in a long run.

Neely Moldovan

Yes we have always had savings auto deduct every month! WE don’t even have to think about it!

Michael

Yes to setting aside from the moment you have your money. It is so effective. This is also what I do on my Tithes! =)

Nicole P.

There was this one time I bought shoes for 500 pesos. Unfortunately, it was wrecked before the month was out. Buying good quality vs the cheaper ones really is the way to go, especially if we’re talking garments or shoes since fashion always recycles itself anyway.

Fransic verso

Great tips, definitely these are very important and I’m working on it as well. Thank you for sharing them!

Rose Ann Sales

Same here! Since the kids also stayed home during the lockdown, we spent more on groceries and food. I’m having a hard time when it comes to setting aside the savings first it’s the opposite for me, your formula would be helpful to me! This means the world to me.

Kat

Money management is a really important life skill and those are all great tips to start. I totally agree with getting quality products as it will save you a lot in the long run.

Blair Villanueva

Delayed gratification is another good strategy for saving money. Living in chosen lifestyle bubble of thriftiness also helps a lot, there is nothing wrong or shameful about reusing things or buying secondhand!

WanderWoMom

ang hirap din talaga mag save ngayon, especially like for me, right when i have enrolled my son to private school, i had to resign from one of my jobs. so 1 job cant sustain me that much. i need to do extra. but i can totally relate na ang easy easy to splurge nitong nag lockdown tayo hahaha! ready to destash na ako 😀

Ntensibe Edgar

Ah yes, delaying my gratification has always helped me approach saving money with a clearer mind and a long-term plan. It always works for me.

Wendy

i can relate to the delayed gratification part. i hold off what i want by “adding to cart” but not really buying. it just satisfies my want to “buy” something but not really proceed to pay out. the funny thing is, I usually just add to cart cheap items, haha. I don’t do much online shopping here in Jakarta as I did in Seoul.

between my husband and me, he is the financially savvy one. I make the budget and he gives me the monthly allowance for our family. I prefer this kind of arrangement because our finances and our savings are more secure.

Christian Foremost

This is something that I definitely needed to hear. My savings had taken quite a toll after i decided to move out, but now it’s more of just figuring out how to get started on saving again. Your tips are super helpful!

An Indian Traveler

These are some really practical and insightful tips. Also, investing the savings is equally (or even more) important by following the general thumb rule of 50(for needs)-30(for wants)-20(for investment) every month.

Karla

I totally agree on spending money on quality products. I don’t mind spending much for something that I know that will last for years.

Michael

No. 1 is the best. Its hard to do at first but when you manage to make it a habit, it’ll do wonders when you need something like for emergencies, etc.. Great tip!

Luna S

Great tips & info! Each month I make a budget of how much we make vs bills & food, then I minus out any extras like hulu/netflix to see what is left and put part of that away into savings + a little info a savings account for both of my kiddos. It really adds up a little bit at a time.

briannemanzb

Spending money on quality products is one good way to save money. This is what I learned the hard way but Im so glad I did.

Will Zeal

Dive into the dynamic world of online gaming, betting, gambling, jackpots, and poker with Will-Zeal blog. Uncover strategic insights for an exhilarating and informed gaming experience.